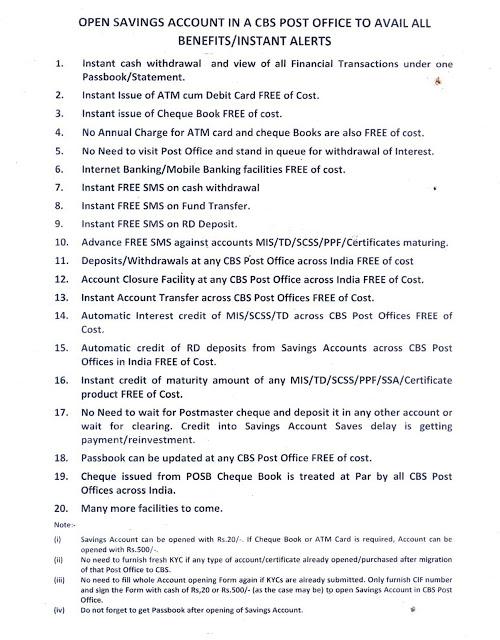

RAJYA SABHA Q&A regarding Post Bank of India & Task force Recommendations on PBI

GOVERNMENT OF INDIA

MINISTRY OF COMMUNICATIONS AND INFORMATION TECHNOLOGY

DEPARTMENT OF POSTS

RAJYA SABHA

UNSTARRED QUESTION NO.163

TO BE ANSWERED ON 24TH APRIL, 2015

POSTAL BANKS

163. DR. PRADEEP KUMAR BALMUCHU:

Will the Minister of COMMUNICATIONS AND INFORMATION TECHNOLOGY be pleased to state:

(a) whether it is a fact that Government is urging the Department of Posts to come up with opening of Postal Banks in the country, if so, the details thereof;

(b) whether the Subramanian Committee, to which the matter had been referred, has submitted its report and has made recommendations in this regard; and

(c) if so, the details thereof?

ANSWER

THE MINISTER OF COMMUNICATIONS AND INFORMATION TECHNOLOGY

(SHRI RAVI SHANKAR PRASAD)

(a) Sir, the Department of Posts has submitted an application to Reserve Bank of India on 30.1.2015 seeking license for setting up Post Bank of India under the rubric of “Payments Bank”. The Government is committed to increasing access of the people to the formal financial system and in this context, Government proposes to utilize the vast Postal network with nearly 1, 54,000 points of presence spread across the villages of the country. The Government hopes that the Postal Department will make its proposed Payments Bank venture successful so that it contributes further to the Pradhan Mantri Jan Dhan Yojana. The details of the proposed Post Bank would be finalized once the Reserve Bank of India takes a favourable decision on application submitted by Department of Posts. In the recent budget speech also the Finance Minister has appreciatingly talked about Post Bank.

(b) & (c ) The Task Force on Leveraging the Post Office Network under the Chairmanship of retired Cabinet Secretary Shri. T.S.R.Subramanian, has submitted its report during November-2014. The said task force has recommended for setting up Post Bank of India. The details of the recommendations are reproduced in theAnnexure- ‘A’ enclosed herewith.

Annexure-A

Recommendations of Task Force on Leveraging Post Office Network with respect to Setting up of Post Bank of India:-

(i) The proposal is not to convert the PO Network into a Bank, but to set up a fully professional new Bank to further financial inclusion and meet the objectives of the Pradhan Mantri Jan Dhan Yojna, which specifically provides for the extension of credit to all Indians resident in every part of India, particularly in rural areas.

(ii) This opportunity for achieving universal financial inclusion via technology and the institutional reach of the PO Network must not be lost. There is admittedly a risk involved, as there is in any new venture into uncharted waters. The risk involved can and must be managed in the interests of the overall larger national objectives.

(iii) The PBI must be professionally managed and operated, with credit and other risks being handled by experienced experts hired from the market. In its own interest, its operations must be fully in line and compliant with RBI Guidelines.

(iv) A new institution, to be called the Post Bank of India or by some other suitable name, should be set up as a commercial bank offering the full spectrum of financial and banking services.

(v) As the owner of the proposed PBI, the Government of India may take decisions as appropriate on structural and organizational issues and other details, including the funding requirements.

(vi) The Task Force is of the view that the PBI should be set up under an Act of Parliament and that establishing the PBI as a statutory institution and a Government Bank would enhance its credibility, insulate it from local pulls and greatly facilitate its operations.

(vii) It is essential to structure the proposed PBI in such a manner as to pre-empt the possibility of outside interests influencing its day-to-day operations.

(viii) The Task Force also recommends that the PBI should initially be set up as a Public Sector Bank wholly owned by the Government of India.

(ix) The initial capital requirement, estimated at Rs. 500 crores as per RBI requirements would be fully funded by the Government.

(x) After the Bank establishes itself in 3 to 5 years, the Board of Directors could take a view on floating an IPO to raise fresh capital.

(xi) The PBI will focus on fulfilling the Government’s mandate of financial inclusion and on bringing the un-banked and under-banked segments of the population, particularly in rural, semi-rural and remote areas within the ambit of the formal monetized economy.

(xii) A view needs to be taken on how best to seamlessly integrate the earlier banking operations into the proposed new structure, The best and seamless method would be to fully absorb the POSB in the new proposed Bank (PBI).

(xiii) The PBI will offer services including credit, which are beyond the remit of the POSB.

(xiv) The PBI will develop financial products and services which are specially tailored to the needs of the rural and urban unbanked population, if necessary in collaboration with other banks.

(xv) The PBI will function as a commercially viable and self-sustaining entity without the need for continuing Government subsidies.

(xvi) After the Initial gestation period, it should generate its own resources and sustain itself in the competitive market environment.

(xvii) The PBI should price its services on a cost plus basis and revise these rates from time to time, so that its operations do not become a continuing and increasing burden on the Government exchequer.

(xviii) The PBI will start with a Head Office Main Branch and will thereafter expand its operations by opening Branch offices in the Metro towns and State capitals, to be manned by banking professionals.

(xix) The longer term objectives would be to establish a Branch Office of the PBI in each District Headquarter over a 3 to 5 year period, to be operated mostly by banking professionals.

(xx) The 150,000-plus Departmental and Branch POs will act as Banking Correspondents for the PBI.

(xxi) Careful consideration should be given to the various types, elements and levels of risk involved in the PBI’s operations.

(xxii) Robust System Protocols and Standard Operating Procedures should be put in place to manage these risks effectively.

(xxiii) The PBI should recruit/commission the services of banking experts to manage its credit, portfolio and market risks.

(xxiv) Appropriate management capabilities should be mobilized from the market and robust systems and processes should be put in place to ensure that Non-Performing Assets are kept within acceptable limits.

(xxv) It is neither necessary nor desirable to mandate a waiting period before the PBI enters into credit and lending operations.

(xxvi) The PBI should be constituted and begin working as a credit and lending Bank immediately, without any trial/waiting/learning period.

(xxvii) The PBI should be set up as an independent Statutory and corporate entity offering the full bouquet services, including credit, to its customers.

(xxviii) The PBI will primarily target currently unbanked and under-banked customers in rural, semi-rural and remote areas, with a focus on providing small and affordable loans and simple deposit products.

(xxix) Customers will be provided with full-fledged Savings Accounts, which can be retained even with zero balances, as provided for in the PMJDY.

(xxx) Credit risks will be managed by hiring professionals from the banking sector and by developing and implementing robust protocols for building checks and balances in the system. Market and robust systems and processes should be put in place to ensure that Non-Performing Assets are kept within acceptable limits.

Comments

Post a Comment